By Channamallikarjun B.Patil

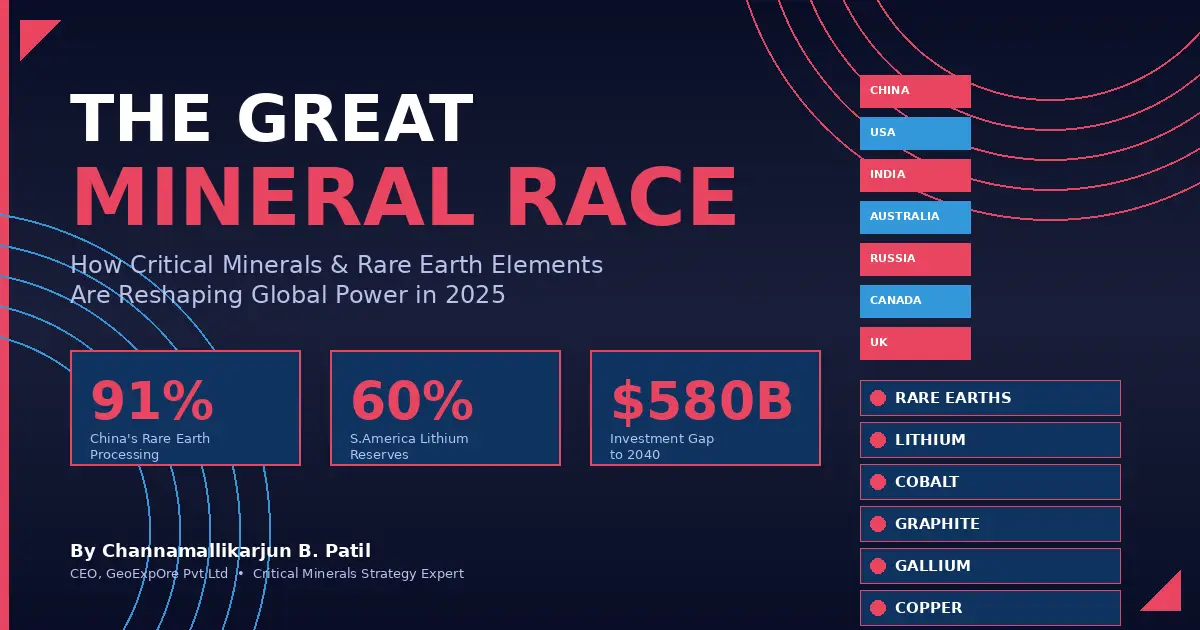

The global race for critical minerals and rare earth elements has become the defining geopolitical contest of our era—eclipsing oil as the resource most likely to reshape alliances, trigger trade wars, and determine which nations lead the clean energy transition. China’s near-monopoly on processing, controlling 91% of rare earth refining and 85% of battery-grade graphite, has transformed these obscure elements into instruments of strategic leverage, prompting an unprecedented scramble by Western democracies to secure alternative supplies. The stakes are existential: without these minerals, there are no electric vehicles, no wind turbines, no advanced fighter jets, and no smartphones.

This tectonic shift became unmistakably clear in late 2024 when Beijing banned exports of gallium, germanium, and antimony to the United States, and again in April 2025 when China imposed licensing requirements on seven heavy rare earth elements essential for permanent magnets. The restrictions sent shockwaves through global supply chains, with European rare earth prices reaching six times Chinese domestic levels within months. Discovery Alert Against this backdrop, nations from Australia to Argentina are positioning themselves as alternative suppliers, while geopolitical alignments—including a surprising India-Russia critical minerals partnership—are being forged with resource security as the primary objective.

Why seventeen elements you’ve never heard of control the future

Critical minerals are non-fuel minerals essential to modern economies whose supply chains face significant disruption risks. The United States currently lists 60 minerals as critical, while the European Union identifies 34, with 17 designated as “strategic.” At the heart of this list are the rare earth elements—a family of 17 metallic elements that, despite their name, are not geologically rare but are rarely found in economically exploitable concentrations.

The rare earths divide into two categories with vastly different strategic implications. Light rare earths like neodymium and praseodymium are essential for the permanent magnets powering electric vehicle motors and wind turbines—an EV requires approximately 2-3 kilograms of rare earth magnets. Heavy rare earths like dysprosium and terbium, far scarcer and almost entirely processed in China, are irreplaceable additives that allow these magnets to function at high temperatures without demagnetizing.

Beyond rare earths, the critical minerals universe encompasses lithium and cobalt for batteries, graphite for anodes, copper for electrification, gallium and germanium for semiconductors, and antimony for ammunition and flame retardants. World Population Review The International Energy Agency projects that demand for these minerals will triple by 2040 under net-zero scenarios, with lithium demand alone increasing ninefold. IEA The aggregate market value of energy transition minerals, currently around $325 billion, is projected to reach $770 billion by 2040— IEAcomparable to the entire iron ore market today.

The defense implications are equally profound. A single F-35 fighter jet requires 920 pounds of rare earth materials. Every precision-guided missile, radar system, night-vision device, and military satellite depends on these elements. The United States remains 100% import-dependent for 12 critical minerals and more than 50% dependent for 28 others, creating what defense analysts describe as a fundamental vulnerability in American military readiness.

Trump’s aggressive push for “mineral dominance”

The Trump administration has made critical minerals a cornerstone of its national security strategy, launching what officials describe as an effort to establish America as the “leading producer and processor of non-fuel minerals.” The approach represents a dramatic departure from the previous administration’s emphasis on allied cooperation, prioritizing instead bilateral deals, tariff pressure, and unprecedented government intervention in mineral markets.

The foundational executive order, “Unleashing American Energy,” signed on January 20, 2025, directed agencies to identify federal lands rich in minerals, streamline permitting, and reassess public land withdrawals that limit mining access. White House Section 9 of the order specifically addressed “Restoring America’s Mineral Dominance,” mandating reviews of the National Defense Stockpile and directing the Secretary of State to explore mineral cooperation through the Quad alliance. White HouseAmerican Foreign Service Association

Two months later, the administration invoked emergency powers through an executive order titled “Immediate Measures to Increase American Mineral Production,” delegating Defense Production Act authority to the Secretary of Defense for domestic mineral production. Perkins CoieThe White House This unprecedented step authorized the Development Finance Corporation—traditionally focused on international projects—to make loans for domestic mineral development, Atlantic CouncilCenter for Strategic and International Studies while directing the Interior Department to prioritize mining as the primary use for federal lands identified as mineral-rich.

The investment commitments have been substantial. The Department of Defense purchased a $400 million equity stake in MP Materials, the operator of California’s Mountain Pass rare earth mine, becoming the company’s largest shareholder with a 15% position. The deal included a 10-year price floor of $110 per kilogram for neodymium-praseodymium products—nearly double current market prices—and a guaranteed purchase commitment for 100% of the company’s future magnet production. Combined with $1 billion in private financing from JPMorgan Chase and Goldman Sachs, the arrangement aims to create America’s first fully integrated rare earth supply chain from mine to magnet.

The “One Big Beautiful Bill Act,” signed on July 4, 2025, allocated $2 billion for National Defense Stockpile expansion and $5 billion for an Industrial Base Fund focused on critical mineral supply chains. The Defense Logistics Agency has issued contracts exceeding $1 billion for antimony, tantalum, niobium, and scandium, while the Department of Energy announced nearly $1 billion in funding opportunities for critical mineral processing, battery manufacturing, and rare earth element domestic supply chain enhancement. Department of Energy

On the diplomatic front, the administration has pursued transactional mineral agreements with striking aggressiveness. The December 2025 “Washington Accords” brokered a peace deal between the Democratic Republic of Congo and Rwanda that included bilateral mineral agreements granting U.S. companies preferential access to gold, tin, tungsten, tantalum, cobalt, and copper. A separate April 2025 agreement with Ukraine established a Reconstruction Investment Fund giving American firms priority access to approximately 100 Ukrainian mineral deposits. Deals with Kazakhstan ($1.2 billion), Pakistan ($500 million), and a $3 billion framework with Australia have followed in rapid succession.

Beijing’s mineral weapon: From dominance to deployment

China’s control over critical mineral supply chains represents one of the most consequential concentrations of economic power in modern history. The country mines 60-70% of global rare earths and processes approximately 91%—a stranglehold built over three decades through state subsidies, lax environmental enforcement, and strategic patience that drove Western competitors from the market. China’s dominance extends across virtually every critical mineral: Discovery Alert 99% of battery-grade graphite, 73% of refined cobalt, 67% of refined lithium, and 98% of gallium production.

This position did not emerge by accident. In 1992, Deng Xiaoping famously declared, “The Middle East has oil, China has rare earths,” signaling Beijing’s intent to leverage these resources strategically. Through the 1990s and 2000s, Chinese producers systematically undercut global competition, contributing to the closure of America’s Mountain Pass mine in 1997 and the collapse of rare earth processing capacity throughout the Western world. Visual Capitalist By 2011, China controlled 97% of global rare earth production.

Beijing has demonstrated its willingness to weaponize this dominance. During the 2010 Senkaku/Diaoyu Islands dispute, China imposed an unofficial embargo on rare earth exports to Japan, The Strategist causing global prices to spike tenfold within a year. While a 2014 WTO ruling forced China to drop formal export quotas, the episode crystallized global awareness of supply chain vulnerabilities—and prompted Japan to reduce its Chinese rare earth dependence from 90% to approximately 60% through efficiency measures and supply diversification.

The recent escalation marks a more systematic deployment of mineral leverage. Beginning with July 2023 export licensing requirements on gallium and germanium—essential for semiconductors—China has progressively expanded restrictions in direct response to American technology export controls. ORF Online The December 2024 outright ban on gallium, germanium, and antimony exports to the United States came one day after Washington expanded chip export restrictions. April 2025 saw licensing requirements imposed on seven heavy rare earth elements critical for permanent magnets, ORF Online while October 2025 brought expanded controls on rare earth processing equipment, permanent magnets, and lithium battery materials.

Most significant was the introduction of a “foreign direct product rule” requiring export licenses for any products worldwide containing more than 0.1% Chinese-origin rare earths— CNNPillsbury Winthrop Shaw Pittmana provision that, if enforced, would affect virtually every electric vehicle, wind turbine, and advanced weapons system on the planet. Within two months of the April 2025 restrictions, some automakers faced critical shortages and paused production lines. Discovery Alert

The June 2024 enactment of China’s Rare Earth Management Regulations formalized state control over the sector, Faegre Drinker declaring all rare earth elements as state property, implementing mandatory traceability systems, and consolidating the industry under two state-owned giants that control 89% of global refining capacity. China has simultaneously accelerated overseas acquisitions, The Strategist investing over $10 billion in African mining assets since 2023 and controlling 72% of copper and cobalt mines in the Democratic Republic of Congo.

A November 2025 trade truce following the Xi-Trump meeting in Busan suspended the most stringent export controls until November 2026, but the legal framework remains intact and can be reactivated instantly. The message to the world is clear: access to critical minerals flows through Beijing, and that access can be terminated at China’s discretion.

India awakens: The National Critical Mineral Mission

India has emerged as a significant new player in the critical minerals arena, launching the ambitious National Critical Mineral Mission in January 2025 with a ₹34,300 crore ($4 billion) commitment over seven years. The initiative reflects New Delhi’s recognition that its clean energy and manufacturing ambitions—including plans to produce 30% of the world’s electric vehicles by 2030—cannot succeed while remaining 100% dependent on imports for lithium, cobalt, nickel, and nine other essential minerals.

The scale of India’s vulnerability is striking. China supplies 82% of India’s lithium imports, 86% of its bismuth, and 76% of its silicon— Policy Circledependencies that Beijing’s recent export controls have exposed as strategic liabilities. India’s annual import bill for lithium alone exceeds ₹24,000 crore ($2.9 billion), and China’s April 2025 rare earth restrictions directly impacted Indian manufacturers reliant on imported permanent magnets.

The National Critical Mineral Mission targets domestic production of at least 15 critical minerals by 2031, completion of 1,200 exploration projects, acquisition of 50 overseas mining assets, and establishment of a National Critical Minerals Stockpile. The discovery of 5.9 million tonnes of lithium in Jammu and Kashmir in 2023 offered encouragement, though India lacks the processing infrastructure to convert raw deposits into usable battery-grade materials.

India’s state-owned overseas acquisition vehicle, Khanij Bidesh India Limited (KABIL), has moved aggressively to secure foreign supplies. A January 2024 agreement with Argentina’s CAMYEN secured exploration rights to five lithium brine blocks ORF Online covering 15,703 hectares in Catamarca Province, representing the first lithium project by an Indian government company. Partnerships with Australia’s Critical Minerals Office have identified five target projects—two lithium and three cobalt—for joint development with $6 million in shared funding.

The July 2025 Quad Critical Minerals Initiative marked a significant multilateral step, bringing India together with the United States, Australia, and Japan to coordinate supply chain diversification, e-waste recovery, and joint stockpiling. East Asia Forum India’s admission to the Minerals Security Partnership IEEFA in 2023—as the first developing country member—and an October 2024 MoU with the United States on critical minerals supply chains signal New Delhi’s integration into Western-aligned supply chain restructuring efforts.

The Putin pivot: Russia-India critical minerals collaboration

The December 2025 summit between Vladimir Putin and Narendra Modi produced an unexpected development in critical minerals geopolitics: a substantial framework for Russia-India cooperation that positions Moscow as an alternative supplier to Beijing. The “Vision 2030” economic cooperation program identified critical minerals as a key pillar alongside civil nuclear energy, with both leaders emphasizing the partnership’s importance for “secure and diversified supply chains.”

Russia holds 22% of global rare earth reserves—the fifth largest deposits worldwide—across 15 rare earth metals, yet produces only a fraction of its potential due to underinvestment and sanctions-related complications. The August 2025 agreement under the Inter-Governmental Commission formalized cooperation in rare earth and critical mineral extraction, industrial and mining infrastructure, and technology transfer for modern mining techniques, specifically targeting lithium, nickel, cobalt, and rare earth elements.

Research collaborations are already underway between India’s CSIR-Institute of Minerals and Materials Technology and Russia’s JSC Giredmet (a Rosatom subsidiary) on rare metals and rare earth processing. Russian Ambassador Denis Alipov has publicly stated that “Russian enterprises are ready to partner with Indian firms in Russia, and also in joint exploration projects across Asia and Africa.”

India and Russia share 17 minerals on their respective critical lists, creating substantial alignment in strategic priorities. For India, the partnership offers diversification away from Chinese supply chains; for Russia, it represents a path to developing mineral resources with Asian partners as Western investment evaporates under sanctions. The strategic logic is compelling for both parties, though implementation will face challenges including infrastructure limitations, technology gaps, and ongoing geopolitical complications from Russia’s international isolation.

South America’s lithium kingdoms: Three countries, three strategies

South America’s “Lithium Triangle”—Argentina, Bolivia, and Chile—contains approximately 60% of the world’s known lithium reserves, CatalystThinredlines positioning the continent at the center of battery supply chain competition. Yet the three countries have adopted radically different approaches to developing their resources, creating a natural experiment in resource nationalism versus market liberalization.

Chile, the world’s second-largest lithium producer with approximately 49,000 tonnes in 2024, CatalystInvesting News Network has moved toward greater state control under President Gabriel Boric. The April 2023 National Lithium Strategy requires state majority stakes in all future “strategic” lithium projects, with state copper company Codelco securing 50% “plus one share” in a restructured partnership with incumbent producer SQM. Catalyst Under the arrangement, the government will receive 85% of the partnership’s operating margin by 2031. The nationalization approach has complicated foreign investment, though Chinese firms—including Tianqi Lithium, which holds 22% of SQM—remain deeply embedded in Chilean lithium exports, with 80% of SQM’s sales flowing to China.

Argentina has pursued the opposite strategy under President Javier Milei, implementing market-friendly reforms designed to attract foreign investment. The December 2024 Rio Tinto announcement of a $2.5 billion investment in the Rincon lithium mine—targeting 60,000 tonnes annual capacity—validated this approach. MINING.COM The RIGI (Regime for Large Investments) law enshrines tax and currency benefits for mining for 30 years, Mining Weekly while Decree 274/2024 slashed mining royalties from 8% to 4% for projects exceeding $500 million. Discovery Alert Argentina’s lithium production surged 62% year-over-year in 2024 Thinredlines to 74,000 tonnes, with a target of 130,000 tonnes in 2025. UPI

Bolivia possesses the world’s largest lithium reserves World Population Review at 21-23 million tonnes but has failed to translate this geological advantage into production, managing only approximately 600 tonnes annually—less than 1% of global output. World Population Review The state-controlled model through Yacimientos de Litio Bolivianos insists on 51% government stakes that deter private investment, while technical challenges with the Uyuni salt flat’s unique chemistry have frustrated extraction efforts. Chinese company CATL subsidiary CBC has signed a $1 billion contract for two plants, S&P Global Commodity Insights but political instability and congressional gridlock have delayed approvals.

Copper presents a parallel story of regional significance. Chile remains the world’s largest producer with 5.5 million tonnes in 2024 (24% of global output), though this share has declined from 33% in 2011 Plusminingplusmining as aging mines face declining ore grades. Peru, historically the second-largest producer, has slipped to third behind the Democratic Republic of Congo, Plusmining with production falling to 2.6 million tonnes amid social conflicts and community blockades affecting operations like MMG’s Las Bambas (Chinese-owned).

Chinese investment in South American lithium has exceeded $16 billion since 2018, Thinredlines encompassing stakes in Chilean, Argentine, and Bolivian operations. The United States has responded through the Minerals Security Partnership, admitting Argentina and Peru as forum members in 2024, Llnl but American influence in the region’s mineral sector remains limited compared to Beijing’s entrenched position.

Australia: From dig-and-ship to mineral superpower

Australia has positioned itself as the indispensable partner for Western critical mineral supply chain diversification, leveraging its status as the world’s largest lithium producer and fourth-largest rare earth producer to attract unprecedented government and private investment. The country’s strategy represents a deliberate evolution from raw material exports toward domestic processing and refining—a shift from “dig and ship” to value-added production.

The numbers underscore Australia’s resource advantage: 88,000 tonnes of lithium production in 2024 Investing News Network (47% of global output), Nasdaq 13,000 tonnes of rare earths (fourth globally), Business News and top-five positions in 21 commodities including cobalt, manganese, tungsten, and nickel. Crucially, Australia leads the world in rare earth exploration investment, securing $64 million (45% of worldwide spending) in 2024 and hosting 89 active exploration projects compared to 18 in Canada and 12 in the United States. Center for Strategic and International Studies

The October 2025 US-Australia Critical Minerals Framework represents the most significant bilateral minerals agreement in recent history, Second Line of Defense establishing an $8.5 billion pipeline of priority projects with immediate commitments of at least $1 billion from each government. The deal includes joint investment in mining and processing, Center for Strategic and International Studies price floors to protect against Chinese market manipulation, coordinated review of Chinese mining asset acquisitions, and streamlined permitting processes. The US Export-Import Bank has issued letters of interest totaling $2.2 billion to seven Australian companies, Center for Strategic and International Studies while a trilateral US-Australia-Japan gallium recovery project at Alcoa’s Western Australia facility Center for Strategic and International Studies could supply approximately 10% of global gallium demand.

Domestically, Australia has committed AU$5 billion through the Critical Minerals Facility (expanded in April 2025) and announced a AU$1.2 billion Critical Minerals Strategic Reserve, Investing News Network expected to become operational in 2026. The February 2025 passage of the Future Made in Australia legislation established a 10% refundable tax offset on critical mineral processing costs, available from 2027-28 through 2039-40.

Lynas Rare Earths, the largest separated rare earths producer outside China, opened Australia’s first domestic rare earths processing plant in Kalgoorlie Global Mining Review in November 2024—an AU$800 million investment processing up to 84,000 tonnes of concentrate annually. The company targets production of 10,500+ tonnes of neodymium-praseodymium annually by 2026. Iluka Resources is developing Australia’s first fully integrated rare earths refinery at Eneabba with AU$1.65 billion in government loans, expected to produce both light and heavy rare earth oxides by 2027.

Australia has simultaneously tightened restrictions on Chinese investment through the Foreign Investment Review Board, The Strategist blocking multiple acquisition attempts McCullough Robertson and issuing an unprecedented divestment order in June 2025 requiring five Chinese-linked investors to sell their stakes in Northern Minerals, a heavy rare earth developer. The message is clear: Australian critical minerals will flow to allied nations, not strategic competitors.

Canada: North America’s mineral anchor under pressure

Canada’s critical minerals sector has assumed heightened strategic importance as trade tensions complicate the integrated North American supply chain that both countries have relied upon for decades. The country ranks among the top five global producers of 10 critical minerals—including potash, niobium, uranium, and nickel—and hosts over 14 million tonnes of rare earth reserves among the largest known deposits worldwide.

The Canadian Critical Minerals Strategy, backed by approximately $3.8-4 billion in federal funding, prioritizes economic growth, Indigenous reconciliation, and partnerships with allies. Export Development CanadaCanada.ca The $1.5 billion Critical Minerals Infrastructure Fund supports clean energy and transportation infrastructure, Canada.ca while tax credits provide 30% for critical mineral exploration and 30% for clean technology manufacturing involving critical minerals extraction, processing, or recycling.

Canada’s integration with the United States is exceptionally deep: International Energy Agency $38 billion in mineral exports to America in 2023 (two-thirds of Canada’s total mineral exports), Columbia University supply of 13 of 35 minerals the U.S. deems critical, Canada.ca and 298 Canadian mining companies operating in the United States. International Energy Agency The first joint US-Canada critical minerals investment, announced in 2024, provided combined funding to Fortune Minerals for its Northwest Territories bismuth-cobalt-copper project. Canada.caCanada.ca

The electric vehicle supply chain has attracted particular attention, with announced investments exceeding $46 billion Pbo-dpb including major battery manufacturing facilities from Stellantis-LG Energy Solution, Volkswagen PowerCo, and Honda Canada. BloombergNEF ranked Canada first globally for battery supply chain potential in 2024, citing the country’s mineral resources, stable governance, and environmental standards. Invest in Canada

Yet the sector faces significant challenges. The Mark Carney government’s March 2025 budget established a $2 billion Critical Minerals Sovereign Fund and $1.5 billion First and Last Mile Fund, while also positioning critical minerals as central to national security rather than solely clean energy transition. Policy Options Trump administration tariffs have complicated cross-border trade, with critical minerals subject to 10% IEEPA tariffs that Canadian officials estimate will add $7.5 billion in annual costs. Columbia University

Canada has taken aggressive action against Chinese investment, ordering three Chinese firms to divest from Canadian lithium companies in November 2022 Holland & KnightThe Standard and continuing to scrutinize acquisitions under strengthened Investment Canada Act provisions. The policy reflects recognition that Canada’s minerals represent a strategic asset whose development must align with allied interests.

Britain’s recycling gambit and the global supply chain puzzle

The United Kingdom faces a critical minerals challenge distinct from resource-rich nations: 100% import dependence for lithium and limited domestic deposits compared to major producers. The November 2025 “Vision 2035” strategy acknowledges this reality while pursuing an ambitious target of 10% domestic production by 2035, primarily through lithium extraction in Cornwall and substantial expansion of recycling capacity.

Cornish Lithium’s Trelavour hard rock project, designated as a Nationally Significant Infrastructure Project, could produce 10,000 tonnes of battery-grade lithium hydroxide annually by 2027, with combined hard rock and geothermal operations potentially reaching 25,000 tonnes by 2030—approximately 25% of projected UK lithium demand. The National Wealth Fund has invested £31 million in Cornish Lithium and £28.6 million in Cornish Metals for tin mining, while total government-backed support for the sector exceeds £165 million. BM Magazine

The UK’s more distinctive contribution lies in recycling and magnet production. HyProMag’s Birmingham facility, which commenced commercial operations in early 2025, represents the first commercial-scale rare earth magnet recycling plant using hydrogen processing technology developed at the University of Birmingham. Maginito Limited. The process requires 88% less energy than primary mining Power Technology and produces the first domestically manufactured sintered magnets in the UK in over 20 years. Maginito Limited. The strategy targets 20% of critical minerals demand met through recycling by 2035.

Britain has pursued bilateral partnerships with nine countries including Australia, Canada, South Africa, Kazakhstan, and Indonesia, while participating in the Minerals Security Partnership as a founding member. The UK hosted the MSP Principals’ meeting at the London Metal Exchange in October 2023 and participates in the MSP Finance Network launched in September 2024.

The race that will define the century

The global critical minerals landscape reveals a fundamental asymmetry that will take decades to address. China’s dominance—91% of rare earth refining, near-monopoly on graphite processing, majority positions across battery materials—was constructed over thirty years and cannot be replicated quickly. The International Energy Agency’s assessment is sobering: diversification efforts are “moving too slowly,” with supply chain concentration actually increasing rather than decreasing in recent years. World Resources Institute The average market share of the top three refining nations rose from 82% in 2020 to 86% in 2024. IEA

Western nations face a $580 billion investment requirement by 2040 to develop alternative supply chains, but low mineral prices—lithium has fallen 75% IEA from 2023 peaks—are deterring the private capital necessary to fund new projects. www Most nickel producers outside the top three suppliers have costs exceeding 2024 prevailing prices, making new capacity additions economically unviable without government support.

The timelines are daunting. New mining projects require 15-18 years on average from discovery to production. Even with accelerated permitting, the first wave of IRA-funded American processing facilities will not reach production until 2027 at the earliest, and meaningful domestic rare earth supply cannot materialize before 2028-2030. The IEA projects that by 2035, copper supply may meet only 70% of demand and lithium only 50%—shortfalls that could derail electric vehicle adoption and renewable energy deployment worldwide.

Yet the competition continues to intensify. China’s Belt and Road Initiative has directed $57 billion to 19 countries for critical mineral extraction, with African investment reaching all-time highs in 2024. The Minerals Security Partnership now includes 15 partner nations plus the European Union, with 15 resource-rich countries participating in its Forum, while bilateral deals multiply between Western capitals and mineral-rich nations from Kazakhstan to the Democratic Republic of Congo.

The critical minerals contest encompasses elements of Cold War-style great power competition, nineteenth-century resource imperialism, and twenty-first-century clean energy transition all simultaneously. Nations that secure reliable access to these materials will lead the industries of the future—electric vehicles, renewable energy, advanced computing, and military systems. Those that fail will find themselves dependent on competitors for the building blocks of modern civilization.

The race is on. The outcome remains profoundly uncertain.

Channamallikarjun B.Patil Founder of GeoExpOre and EarthScience.AI